Executive Summary

The Patient Protection and Affordable Care Act(1) requires the Secretary of Labor to provide Congress with an annual report containing general information on self-insured employee health benefit plans and financial information of employers that sponsor such plans. The report must use data from the Annual Return/Report of Employee Benefit Plan (Form 5500), which many self-insured health plans must file annually with the Department of Labor. Congress received the first report in March 2011.(2)

Along with this report, the Department is submitting two detailed appendices:

Appendix A, Group Health Plans Report: Abstract of 2023 Form 5500 Annual Reports Reflecting Statistical Year Filings, provides detailed statistics describing group health plans that file a Form 5500.(3)

Appendix B, Self-Insured Health Benefit Plans 2026: Based on Filings through Statistical Year 2023, explores statistical issues associated with Form 5500 health plan data and analyzes available data on the financial status of employers that sponsored group health plans and filed the Form 5500.(4)

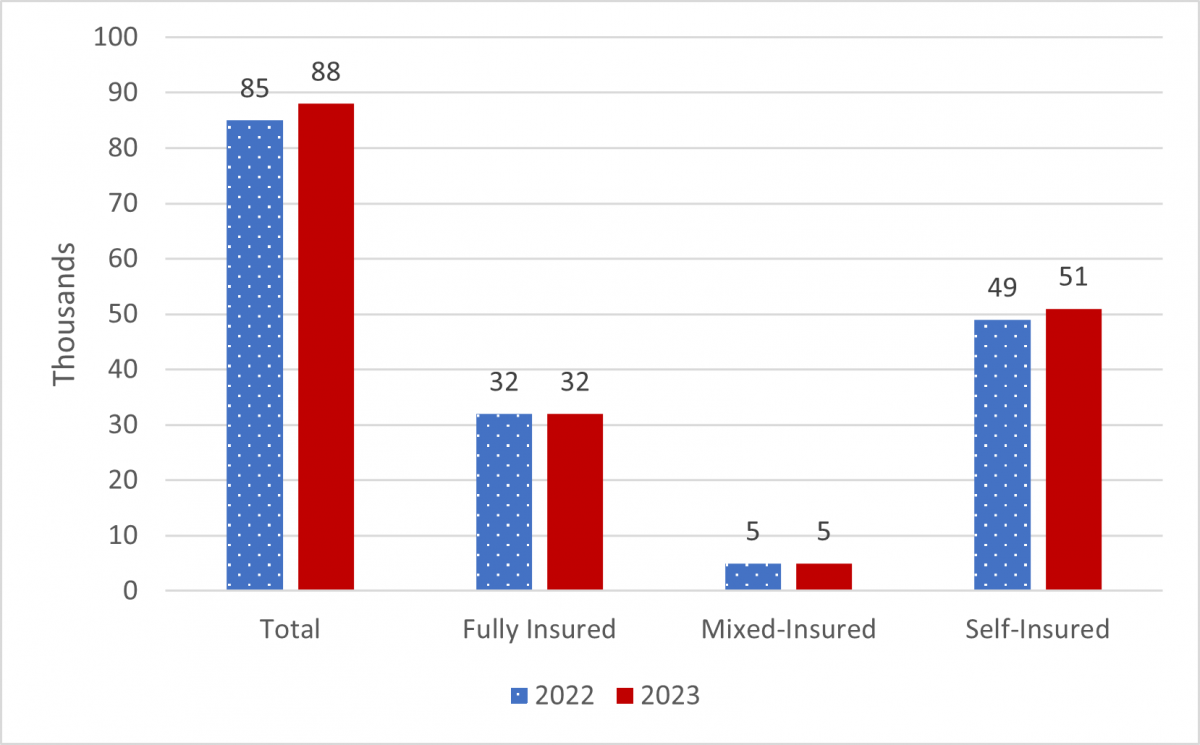

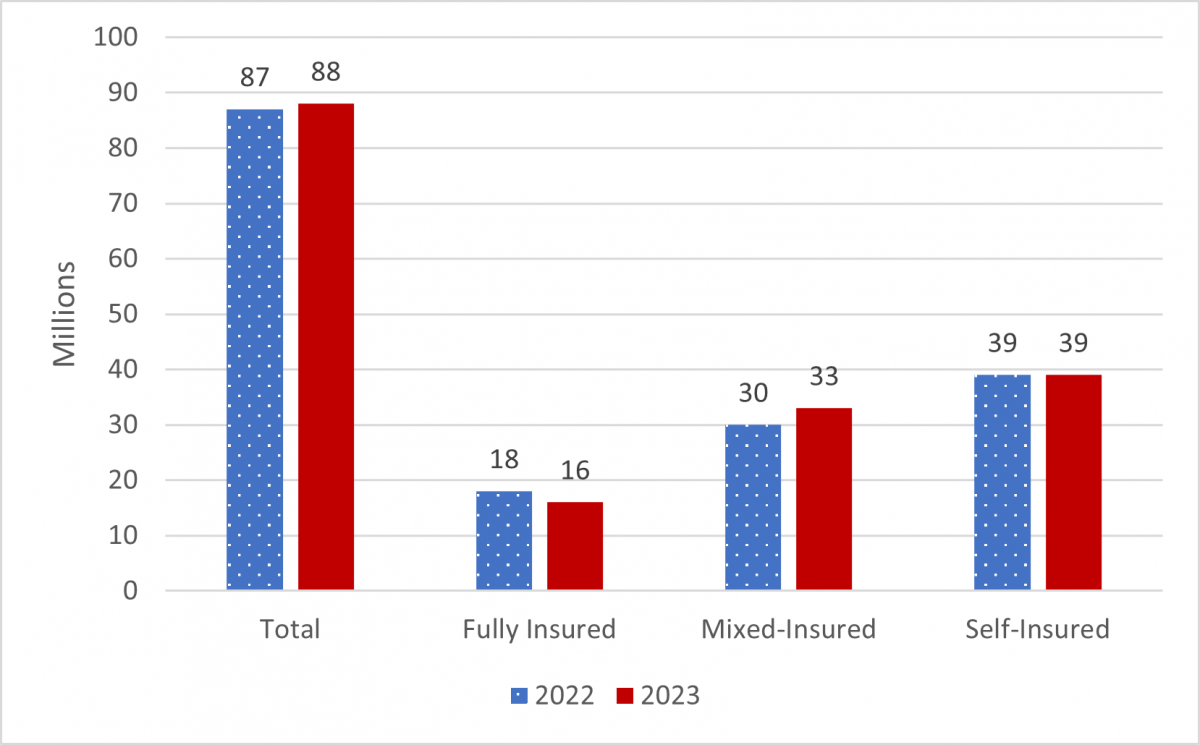

This report presents data on private-sector employer health benefit plans’ Form 5500 filings for statistical year 2023, the latest year for which complete data are available. Approximately 87,706 group health plans filed a Form 5500 for 2023, an increase of 3 percent from 2022. Of those plans, about 50,700 were self-insured, and 4,800 mixed self-insurance with insurance (“mixed-insured”). Self-insured plans covered nearly 39 million participants and held approximately $128 billion in assets, while mixed-insured plans covered approximately 33 million participants and held about $142 billion in assets.

Table 1 summarizes aggregate statistics on plan counts, participants, and assets for self-insured and mixed-insured group health plans that filed a Form 5500 for statistical years 2022 and 2023.

| Plan Type | 2022 | 2023 | ||

|---|---|---|---|---|

| Self-Insured Plans | Mixed-Insured Plans | Self-Insured Plans | Mixed-Insured Plans | |

| All Plans | 48,700 | 4,700 | 50,700 | 4,800 |

| Participants | 39 million | 30 million | 39 million | 33 million |

| Active Participants† | 34 million | 27 million | 34 million | 29 million |

| Large Plans‡ Not Holding Assets in Trusts | 20,000 | 4,000 | 20,800 | 4,000 |

| Participants | 25 million | 25 million | 26 million | 26 million |

| Active Participants | 23 million | 23 million | 24 million | 24 million |

| All Plans Holding Assets in Trust | 28,700 | 800 | 29,900 | 800 |

| Participants | 13 million | 5 million | 13 million | 7 million |

| Active Participants | 11 million | 4 million | 10 million | 5 million |

| Assets | $120 billion | $135 billion | $128 billion | $142 billion |

| Contributions | $67 billion | $67 billion | $68 billion | $73 billion |

| Benefits | $63 billion | $68 billion | $65 billion | $73 billion |

NOTES: All figures in this table have been rounded.

* The Department defines a “statistical year” Form 5500 filing population as all Form 5500 employee benefit plan filings with a plan year ending date between January 1 and December 31 of a given year.

† See https://www.dol.gov/sites/dolgov/files/ebsa/employers-and-advisers/plan-administration-and-compliance/reporting-and-filing/form-5500/2023-instructions.pdf.

‡ Plans with at least 100 participants.

SOURCE: 2022 and 2023 Form 5500 filings.

Self-insured plan sponsors pay covered health expenses directly (either from their general assets or from a trust) as the plans incur claims. Fully insured plan sponsors generally pay premiums to insurers that assume the responsibility for paying claims. Mixed-insured plan sponsors retain claims-paying responsibility for some benefits but transfer the risk for paying the remaining benefits to insurers, thereby financing benefits using a mixture of self-insurance and insurance. Self-insurance is more common among larger group health plan sponsors, in part because the health expenses of larger group health plans are more predictable, and therefore, larger plan sponsors can better manage those risks internally while avoiding costs associated with state taxes and insurance fees.

Somewhat different rules govern self-insured and fully insured group health plans. For example, the Employee Retirement Income Security Act (ERISA) preempts state laws regarding employee benefit plans, including health plans.(5) However, states have the right to regulate the business of insurance and persons engaged in that business.(6) State insurance laws may not deem an employee benefit plan to be an insurer, but states have jurisdiction over issuers that provide fully insured plans with coverage.

Generally, private-sector employer health benefit plans must file a Form 5500 if they have 100 or more participants. Regardless of size, plans must file a Form 5500 if they hold assets in trust or are identified as a Multiple Employer Welfare Arrangement (MEWA) or certain Entities Claiming Exception (ECE).

Most small (typically fewer than 100 participants), ERISA-covered group health plans do not hold assets in trust and, therefore, are not required to file a Form 5500. As a result, this report excludes a large majority of small health benefit plans – including a potentially significant but unknown number of small, self-insured plans.

The Department estimates that there were about 2.8 million ERISA-covered group health plans covering approximately 135 million participants and beneficiaries in 2023.(7) Only about 87,700 plans covering 88 million participants filed a 2023 Form 5500.(8) Of the group health plans that filed a Form 5500, about 37,000 (42.2 percent) filed at least one Schedule A (Insurance Information) for a group insurance policy covering health benefits,(9) and about 31,300 plans (35.7 percent) reported holding assets and filed a Schedule H (Financial Information) or Schedule I (Financial Information–Small Plan).(10)

The Form 5500 does not collect data on plan sponsors’ finances.(11) However, financial data for a subset of sponsoring employers that issue publicly traded equity or debt are available from other sources.(12) The financial strength of these plan sponsors varies considerably. Employers sponsoring self-insured plans, mixed-insured plans, and fully insured plans show similar variation.

Introduction

Section 1253 of the Patient Protection and Affordable Care Act (the “Affordable Care Act”)(13) requires the Secretary to prepare an aggregate annual report that includes certain general information on self-insured group health plans using data collected from the Annual Return/Report of Employee Benefit Plan (Form 5500),(14) as well as certain data from financial filings of self-insured employers.

There are three categories of group health plans: self-insured plans, fully insured plans, and mixed-insured plans. Self-insured plan sponsors generally pay their plans’ covered health expenses directly, as the plans incur claims. Fully insured plan sponsors typically pay premiums to insurers, which then assume the responsibility for paying claims. Mixed-insured plan sponsors are responsible for paying some benefits but transfer the risk for the other benefits to health insurers—that is, they finance benefits using a mixture of self-insurance and insurance.

The Form 5500 does not explicitly disclose whether a health plan is self-insured. However, there are key qualitative differences between the three plan categories,(15) so the Department created an algorithm using filing characteristics to sort plans as self-insured, fully insured, or mixed-insured.

The Department’s first report was issued in March 2011. Significant revisions were made to the methodologies for determining the plan universe for analysis and the funding mechanisms of group health plans in the March 2013 report. The methodology surrounding plans’ funding mechanisms has continued to evolve since the March 2013 report. The Department uses its current methodologies to incorporate previous years’ data into this report to facilitate comparisons over time.(16) However, because past reports may have relied on different methodologies, trends over time cannot be identified merely by directly comparing the numbers in prior reports.

In some instances, group health benefits are offered through a plan that provides coverage to the employees of two or more employers (and is not a collectively bargained arrangement). Such a plan generally constitutes a MEWA under ERISA and is required to file a Form 5500 regardless of size or holding of assets. The Department classifies and reports plans according to their sponsor type: single-employer plans, multiemployer(17) plans, and multiple employer plans.(18)

Section I. Required Form 5500 Group Health Plan Data

Section 1253 of the Affordable Care Act requires the Department to submit information on several data items from the Form 5500:

“general information on self-insured group health plans (including plan type, number of participants, benefits offered, funding arrangements, and benefit arrangements)”

“data from the financial filings of self-insured employers (including information on assets, liabilities, contributions, investments, and expenses).”

The Form 5500 data presented below in response to these requirements should be carefully interpreted for several reasons.(19)

The Department has information on these data items only for plans required to file a Form 5500. Generally, private-sector employer group health plans must file a Form 5500 only if they cover 100 or more participants, hold assets in trust, or constitute a plan MEWA. Governmental and church plans, regardless of size, are not subject to the jurisdiction of the Department and are not required to file a Form 5500. Because information on such plans is not available in the Form 5500 data, this report does not include them in its statistics.

Self-insured welfare benefit plans, including group health plans, must generally file financial information only for assets held in trust. Thus, this report understates aggregate financial statistics because it excludes health benefits paid directly from plan sponsors’ general assets. Of the self-insured plans that filed a Form 5500 in 2023, 41 percent did not hold assets in trust and therefore did not report financial information.

In cases where a single plan provides multiple types of welfare and health benefits, it may report these together with other welfare benefits, such as disability or life insurance benefits, on a single Form 5500. This can make it difficult to determine how the different benefits are financed and whether the group health component of the plan is self-insured or fully insured.(20) As a result, this report provides estimates marked by substantial uncertainty.

| Plan Type | All Plans | Self-Insured Plans | Mixed-Insured Plans | Fully Insured Plans* |

|---|---|---|---|---|

| All Plans | 87,700 | 50,700 | 4,800 | 32,200 |

| Participants | 88 million | 39 million | 33 million | 16 million |

| Active Participants | 79 million | 34 million | 29 million | 15 million |

| Large Plans Not Holding Assets in Trusts | 56,400 | 20,800 | 4,000 | 31,600 |

| Participants | 66 million | 26 million | 26 million | 14 million |

| Active Participants | 61 million | 24 million | 24 million | 14 million |

| All Plans Holding Assets in Trust | 31,300 | 29,900 | 800 | 700 |

| Participants | 22 million | 13 million | 7 million | 2 million |

| Active Participants | 17 million | 10 million | 5 million | 2 million |

| Assets | $285 billion | $128 billion | $142 billion | $16 billion |

| Contributions | $157 billion | $68 billion | $73 billion | $16 billion |

| Benefits | $153 billion | $65 billion | $73 billion | $16 billion |

NOTES: All figures in the table have been rounded. Totals may not equal the sum of the components due to rounding.

* Plans that report benefit payments are classified as fully insured only if the Form 5500 filing reports that these payments were made to insurance companies for the provision of benefits and not made directly to participants.

SOURCE: 2023 Form 5500 filings.

Plan Type by Funding Mechanism

Funding mechanism refers to the method a health plan uses to finance its benefits. Plan sponsors may choose to pay for health services directly through the sponsor’s general assets, with plan assets by purchasing insurance to cover benefit obligations, or some combination. For the purposes of this report, the Department classifies those arrangements as “self-insured,” “fully insured,” or “mixed-insured” respectively.

Of the self-insured group health plans:

about 49,400 were sponsored by single employers,

fewer than 1,000 were multiemployer plans, and

fewer than 300 were multiple employer plans.(21)

Of the mixed-insured group health plans:

about 4,500 were sponsored by single employers,

fewer than 300 were multiemployer plans, and

more than 50 were multiple employer plans.(22)

The number of group health plans that filed a Form 5500 increased by 3 percent between 2022 and 2023. Mixed-insured and self-insured plans increased by about 2 percent and 4 percent, respectively.(23) Although the number of self-insured plans increased in 2023, the rate of change was slightly less than in 2022 and significantly less than the greater than 20 percent increases in the number of self-insured plans in 2020 and 2021.(24)

SOURCE: Appendix B, Tables 7 and 16.

Number of Participants

The approximately 50,700 self-insured group health plans covered nearly 39 million participants, 34 million of whom were active participants. The 4,800 mixed-insured group health plans covered nearly 33 million participants, approximately 29 million of whom were active participants.(25)

Plans covering a larger number of participants were more likely to be self-insured or mixed-insured than plans with fewer participants. While roughly 54 percent of large plans were fully insured, they covered only 19 percent of large plan participants.(26)

The number of participants increased by 1 percent between 2022 and 2023. The overall distribution of participants by funding type stayed mostly the same, but there were significant changes within each funding type. Specifically, mixed-insured plans saw a 9 percent increase in participants, while fully insured plans experienced a 10 percent decrease in participants.(27)

SOURCE: Appendix B, Tables 7 and 16.

New Plans

New health plans are defined as health plans that checked the “first return/report filed for the plan” box on their Form 5500 filing.(28) The total number of new plans declined by 7 percent in 2023, driven by a nearly 16 percent decline in new, small, self-insured plans.(29) Of the nearly 8,400 new group health plans, nearly 62 percent were small plans and of those, more than 99 percent of new, small plans were self-insured, driven by an influx of filings from small, self-insured plans participating in non-plan MEWAs.(30)

New, large plans made up 38 percent of all filings, with the number of those fully insured increasing by nearly 14 percent in 2023.(31) Overall, 72 percent of new, large plans were fully insured.

Participants in new, large group health plans were split among funding types:

34 percent were covered by self-insured plans,

14 percent by mixed-insured plans, and

Nearly 52 percent by fully insured plans.(32)

However, 96 percent of participants in new, small plans were covered by self-insured plans.(33)

Funding Mechanisms Over Time

Plans filing a Form 5500 can also be matched across years to track plan changes over time. From 2019 to 2023, on average, 83 percent of plans matched their previous years’ filing.(34) While some plans are consistent in their funding mechanism over time, nearly 11 percent of large, established plans switched their funding type at least once during this period.(35) Large, established plans that change their funding mechanism status were more likely to switch to self or mixed-insured plans than to fully insured plans. Among large, established plans, fully insured plans were slightly more likely to cease filing than plans with a self-insured component.(36,37)

Overall, the number of health plans filing a Form 5500 and the number of participants they cover continues to grow, though their distributions have shifted slightly since 2022. The share of health plans reported in the Form 5500 with some component of self-insurance remained relatively unchanged (63 percent) from 2022 to 2023(38) while the share of participants covered by some component of self-insurance increased from nearly 79 percent to 81 percent.(39)

The growth in the number of plans with a self-insured component appears driven by small, self-insured plans filing a Form 5500, which have increased more than 13-fold since 2014.(40) The majority of those small, self-insured plans participate in a non-plan MEWA. The rate of entry of new, small plans has slowed in recent years, however, decreasing by nearly 16 percent since 2022. Still, those small plans now account for more than half of all self-insured plan filings and 31 percent of all Form 5500 health plan filings in 2023.(41)

Most participants in health plans filing a Form 5500 have some component of self-insurance, primarily because larger plans are more likely to include a self-insured component. In 2023, while 47 percent of large plans were self- or mixed-insured, they covered 81 percent of participants in large plans.(42)

As noted previously, large, established, fully insured plans are more likely to change their funding mechanism over time to mixed- or self-insured than other large, established plans.(43) While large, new plans are somewhat more likely to switch to full insurance, they made up only 5 percent of all large plans in 2023, and so their impact is minimal.(44) Thus, large plans do move, on net, away from full insurance. The nearly 9 percent increase in participants in mixed-insured plans in 2023 was likely caused by a very large plan that switched from fully insured in 2022 to mixed-insurance in 2023.(45)

Benefits Offered

About 28,200 self-insured group health plans offered only health benefits, and about 22,400 offered health and other benefits.(46)

Of the 4,800 mixed-insured plans, about 150 offered only health benefits, and roughly 4,700 offered health and other benefits.(47)

Funding and Benefit Arrangements

Funding Arrangements

A funding arrangement is the method by which the plan receives, holds, invests, and transmits assets that have not yet been used to provide benefits.

Among the self-insured group health plans, approximately:

1,600 indicated a trust-only funding arrangement,

1,400 indicated a funding arrangement of trust with insurance,

3,200 indicated funding from the sponsor’s general assets only,

17,300 indicated funding from the sponsor’s general assets combined with insurance,(48)

1,500 indicated insurance alone(49) or some other combination of funding arrangements, and

25,800 did not report any arrangement.(50)

Among the 4,800 mixed-insured group health plans, approximately:

200 indicated a trust-only funding arrangement,(51)

400 indicated a funding arrangement of trust with insurance,

4,000 indicated funding from the sponsor’s general assets combined with insurance, and

the remaining indicated insurance alone or some other combination of funding arrangements.(52)

Benefit Arrangements

A benefit arrangement is the method by which the plan provides benefits to participants.

Among the self-insured group health plans, approximately:

900 indicated a benefit arrangement of a trust only,

2,000 indicated a benefit arrangement of trust with insurance,

3,000 indicated a benefit arrangement of the sponsor’s general assets only,

17,400 indicated a benefit arrangement of the sponsor’s general assets combined with insurance,(53)

1,600 indicated insurance alone or some other combination of funding arrangements, and

25,800 did not report any arrangement.(54)

Among the mixed-insured group health plans, approximately:

500 indicated a benefit arrangement of trust with insurance,

4,000 indicated a benefit arrangement of the sponsor’s general assets combined with insurance, and

the remaining 200 plans indicated insurance or trust alone, or some other combination of benefit arrangements.(55)

Stop-Loss Insurance

Self-insured plans may purchase stop-loss insurance to mitigate the risk of unexpectedly large medical claims. Stop-loss insurance contracts protect against claims that are catastrophic or unpredictable by covering claim costs that exceed a set amount for either a single enrollee or for aggregate claims over a determined period.

If a sponsor purchases stop-loss insurance for its own benefit, it generally does not need to report the stop-loss insurance on Schedule A (Insurance). As a result, Form 5500 filings often understate the use of stop-loss insurance as part of the sponsor’s arrangement for the plan, especially for plans that do not use a trust.

From 2014 to 2023, the percentage of large group health plans that reported having stop-loss insurance gradually declined, from 26 percent to nearly 20 percent for self-insured plans and from 18 percent to 14 percent for large, mixed-insured plans.(56)

The trend was markedly different for small group health plans. The percentage of small, self-insured plans that reported having stop-loss insurance increased from 23 percent in 2014 to nearly 59 percent in 2023, with a fairly steady growth throughout that period. The percentage of small, mixed-insured health plans reporting stop-loss insurance ranged from 53 percent in 2014 to 51 percent in 2023, though because of the small universe of those plans, the annual share reporting stop-loss insurance tends to be volatile.(57)

Plan Assets and Liabilities of Plans That Financed Benefits through Trusts

Roughly 29,900 self-insured group health plans operated trusts, a 4 percent increase compared with 2022. These plans reported $128 billion in assets (6 percent more than in 2022) and $13 billion in liabilities (the same as 2022).

About 800 mixed-insured group health plans financed benefits through trusts. These plans reported about $142 billion in assets (5 percent more than in 2022) and $19 billion in liabilities (12 percent more than in 2022).(58,59)

Contributions, Investments, and Expenses of Plans That Financed Benefits through Trusts

Contributions & Benefit Payments

Self-insured group health plans that financed benefits through a trust received approximately $68 billion in contributions and paid approximately $65 billion in benefit payments. Of the amount paid, approximately:

$51 billion was paid directly to participants or beneficiaries,

$6 billion was paid to insurance carriers for the provision of benefits,(60) and$7 billion was reported as “other” and cannot be categorized.(61,62)

Mixed-insured group health plans that financed benefits through a trust received approximately $73 billion in contributions and paid approximately $73 billion in benefit payments. Of the amount paid, approximately:

$53 billion was paid directly to participants or beneficiaries,

$17 billion was paid to insurance carriers for the provision of benefits, and

$3 billion was reported as “other” and cannot be categorized.(63)

Administrative Expenses(64)

Self-insured group health plans that financed benefits through a trust reported paying about $4 billion in administrative expenses, with approximately:

$700 million in professional fees,(65)

$2 billion in contract administrator fees,

$200 million in investment advisory and management fees, and

Mixed-insured group health plans that financed benefits through a trust reported paying about $4 billion in administrative expenses, with approximately:

$400 million in professional fees,

$2 billion in contract administrator fees,

$500 million in investment advisory and management fees, and

$1 billion in other administrative expenses.(68)

Asset Holdings(69)

The asset holdings reported by self-insured group health plans with 100 or more participants and who financed benefits through trusts were composed of:

8 percent in cash,

8 percent in U.S. government securities,

6 percent in partnership/joint venture interests,

20 percent in direct filing entities (DFEs),

25 percent in mutual funds (also known as registered investment companies),

9 percent in debt instruments, and

8 percent in stock.(70)

The asset holdings reported by mixed-insured group health plans with 100 or more participants and who financed benefits through trusts were composed of:

7 percent in cash,

15 percent in U.S. government securities,

20 percent in partnership/joint venture interests,

11 percent in DFEs,

11 percent in mutual funds,

21 percent in debt instruments, and

4 percent in stock.(71)

Section II. Additional Analysis of Financial Information on Employers Sponsoring Self-Insured, Mixed-Insured, and Fully Insured Group Health Plans

Section 1253 of the Affordable Care Act requires this report to include data from the financial filings of self-insured employers, including information on assets, liabilities, contributions, investments, and expenses.

Form 5500 filings do not include data on the financial position of the plan sponsor or employer. In order to provide data on financial filings of self-insured employers, Form 5500 data were matched to Bloomberg financial data available for a select group of companies with publicly traded equity or debt.(72) The analysis of financial measures – including revenue, market capitalization, profit, and number of employees – shows that companies offering self-insured or mixed-insured group health plans tend to be larger than companies offering fully insured plans.(73)

The results of matching the 2023 Form 5500 data to the Bloomberg financial data were similar to the results for 2022. Approximately 3,400 Form 5500 filers, or about 6 percent of large plans in the 2023 Form 5500 health plan data, were matched to the Bloomberg data. Because the Bloomberg data represents mostly large, publicly traded companies that are based in the United States, the findings cannot be generalized and applied to smaller, privately held companies or employers participating in multiemployer or multiple employer plans. Of the participants in matched plans, nearly 90 percent were covered through a plan with 5,000 or more participants.(74)

Approximately 1,500 employers matched to a large, self-insured health plan. Employers sponsoring these plans reported a median employee count of nearly 6,500, a median revenue of approximately $2.8 billion, a median market capitalization of nearly $4.6 billion, and a median profit of $216 million.(75)

Roughly 1,000 employers matched to a large, mixed-insured health plan. Employers sponsoring these plans reported a median employee count of 13,800, a median revenue of $5.9 billion, a median market capitalization of approximately $9.0 billion, and a median profit of $348 million.(76)

Similarly, about 900 employers matched to a large, fully insured health plan. These employers tended to be smaller with a median employee count of 1,000, median revenue of roughly $500 million, median market capitalization of $1.2 billion and a median profit of $10 million.(77)

The matched companies’ financial health was measured using three metrics: the ratio of profit to total debt, the ratio of cash and cash equivalent holdings to total debt, and the Altman Z-Score.(78) The distribution of their scores was reported by plan funding type.(79) Overall, the results varied.

Employers sponsoring large, fully insured plans have more cash flow relative to total debt than employers sponsoring mixed- or self-insured plans. As a result, a larger share of employers sponsoring fully insured plans were in the top two categories of the cash/debt measure than employers sponsoring either self-insured or mixed-insured plans. However, a larger share of employers sponsoring fully insured plans had worse scores for operating profit-to-debt ratio as well as worse Altman Z-scores than self-insured or mixed-insured plans.

This variance makes it difficult to draw conclusions regarding a company’s financial health and its choice of funding mechanism for its health plan, particularly as this analysis is limited to large, publicly traded companies. It is noteworthy that, similar to prior years, there was generally greater variation in the financial health of companies sponsoring fully insured plans than self- or mixed-insured plans.

Section III. Conclusion

This annual report provides the most detailed statistics currently available on self-insured group health plans that filed a Form 5500 and on the sponsors of such plans that issue publicly traded equity or debt. This report also documents the limited scope of such data and the complexities involved in interpreting it.

The Department recognizes the importance of quality data and strives to further enhance this report and its underlying statistics to continue to inform Congress about these plans and their sponsors’ financial information.

Footnotes

P.L. 111–148 (Mar. 23, 2010). ↩

Available at https://www.dol.gov/sites/default/files/ebsa/researchers/statistics/retirement-bulletins/annual-report-on-self-insured-group-health-plans-2011.pdf. The 2012–2025 reports are also available online at https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/reports. However, due to changes to the algorithm and methodology beginning with the 2013 report, the reports are not comparable over time. ↩

This work was conducted for the Department by the Actuarial Research Corporation (ARC) under contract number 1605C1-24-F-00051. ↩

This work was conducted for the Department by Advanced Analytical Consulting Group (AACG) under contract number 1605C1-24-C-0021. ↩

ERISA section 514(a) ↩

ERISA section 514(b)(2)(A) ↩

EBSA health plan estimates are based on the 2024 Medical Expenditure Panel Survey, Insurance Component (MEPS-IC), and the 2022 Statistics of U.S. Businesses from the Census Bureau. Participant and beneficiary counts for calendar year 2023 are from Table 3A of the Health Insurance Coverage Bulletin: Abstract for the March 2024 Annual Social and Economic Supplement to the Current Population Survey, https://www.dol.gov/sites/dolgov/files/EBSA/researchers/data/health-and-welfare/health-insurance-coverage-bulletin-2024.pdf. ↩

See Appendix A, Table A1. ↩

See Appendix A, Table B1. ↩

Statistics from Appendix A, Table A2. ↩

For multiemployer plans in particular, the plan sponsor is the association, committee, joint board of trustees, or other similar group of representatives of the parties who establishes or maintains the plan and generally does not have finances separate from the plan. ↩

The analysis in this report relies on Bloomberg data, which uses Form 10-K filings and other sources to collect data on companies with public financial statements and generally includes companies with publicly traded stock or bonds. ↩

P.L. 111–148 ↩

The following welfare plans, including group health plans, are not required to file a Form 5500, due to statutory exemptions from ERISA or regulatory exemptions:

welfare plans (other than plans required to file the Form M-1) with fewer than 100 participants as of the beginning of the plan year (small plans) that are unfunded, fully insured, or a combination of insured and unfunded;

welfare plans maintained outside the United States that serve mostly nonresident aliens;

governmental plans;

unfunded or insured welfare plans maintained for a select group of management or highly compensated employees only;

plans maintained only to comply with workers’ compensation, unemployment compensation, or disability insurance laws;

welfare benefit plans that participate in a group insurance arrangement that files a Form 5500 on behalf of the plan;

apprenticeship or training plans meeting certain conditions;

certain dues financed unfunded welfare benefit plans where certain reports are filed under the Labor-Management Reporting and Disclosure Act;

church plans; and

welfare benefit plans maintained solely for the owner and/or spouse who wholly own a trade or business or the partners and/or spouses of partners in a partnership.

A small plan that (1) receives employee (or former employee) contributions during the plan year and does not use the contributions to pay insurance premiums or (2) uses a trust or separately maintained fund to hold plan assets or act as a conduit for the transfer of plan assets during the year is generally required to file. However, a small plan with employee contributions that are used to pay benefits instead of insurance premiums and is associated with a cafeteria plan under Internal Revenue Code section 125 may be treated as an unfunded welfare plan for annual reporting purposes if it meets certain Department requirements. (See 29 C.F.R. 2520.104-1 et seq.) In addition, plans that are MEWAs required to file the Form M-1 must file the Form 5500, regardless of plan size. See https://www.dol.gov/sites/dolgov/files/EBSA/employers-and-advisers/plan-administration-and-compliance/reporting-and-filing/forms/m1-2023.pdf. ↩

Annual Report on Self-Insured Group Health Plans, Section III, What is a Self-Insured Group Health Plan? (U.S. Department of Labor, March 2011). See https://www.dol.gov/sites/dolgov/files/EBSA/researchers/statistics/retirement-bulletins/annual-report-on-self-insured-group-health-plans-2011.pdf. ↩

Subject to the following criteria, the analysis for this report is based on health benefit plans that filed a Form 5500 or Form 5500-SF.

Test filings, direct filing entity filings (including group insurance arrangements [GIAs], which can only file on behalf of participating plans if they are fully insured and use a trust), duplicative filings, and filings for “one-participant” retirement plans with health plan features have been removed from the raw data set prior to analysis. Because some GIAs provide fully insured group health benefits, the number of participants receiving fully insured group health benefits that are covered by Title I of ERISA and reported on the Form 5500 may be understated. Information on the 47 Health GIAs that filed in 2023 is found in Appendix A of this report.

“Voluntary” filers (i.e., those that appear to meet the exception from the requirement to file based on the information provided but still filed) have been excluded from the analysis. Filers with fewer than 100 beginning-of-year (BOY) participants and no assets held were dropped from the universe, including those with the following fields equal to zero or left blank on their Form 5500-SF or Schedule I or H:

Beginning/End-of-Year Assets, Liabilities, and Net Assets

Income, Expenses, and Net Income

For Form 5500-SF filers with fewer than 100 BOY participants and showing financial information, we have assumed that it was an appropriate filing and that the plan must be self-insured.

Terminating trusts and plans that indicate zero end-of-year (EOY) participants have been included.

For plans with missing EOY participants that are nonterminating, BOY participants have served as a proxy for EOY total and active participants.

A “multiemployer plan” as defined in ERISA section 3(37) is a plan to which more than one employer is required to contribute, and which is maintained pursuant to one or more collective bargaining agreements between one or more employee organizations and more than one employer. ↩

Beginning with the Statistical Year 2017 filings, any plan that self-identifies as a multiple employer plan is classified as a multiple employer plan. In addition, plans that identify as multiemployer plans are reclassified as multiple employer plans if they report a business code of offices of physicians or dentists, real estate, or legal services. Of the 87,700 group health plans in this year’s report, 865 were classified as multiple employer plans. Of those, 265 were self-insured and 55 were mixed-insured. ↩

See the section titled “The Definitions of Funding Mechanisms” in Appendix B for a detailed description of the Department’s method for estimating whether group health plans are self-insured, fully insured, or “mixed-insured,” based on the Form 5500 data. ↩

See report, Strengths and Limitations of Form 5500 Filings for Determining the Funding Mechanism of Employer-Provided Group Health Plans, at https://www.dol.gov/sites/default/files/ebsa/researchers/analysis/health-and-welfare/strengths-and-limitations-of-form-5500-filings-for-determining-the-funding-mechanism-of-employer-provided-group-health-plans.pdf for a discussion of the sensitivity of plans’ funding categorizations. This work was conducted for the Department by Deloitte Financial Advisory Services LLP under task order number DOLB109330993. ↩

For certain Form 5500 reporting purposes, a “controlled group” or affiliated service group under Code section 414(b), (c), or (m) is generally considered a single employer. ↩

See Appendix A, Table A2. ↩

Based on EBSA calculations using 2022 and 2023 Form 5500 filings. ↩

See Appendix B, Tables 7 and 16. ↩

See Appendix A, Table A1. ↩

See Appendix B, Table 14. ↩

See Appendix B, Tables 7 and 16. ↩

Beginning with the 2013 Self-Insured Report to Congress, the Department identified plans as “new” if they checked the “first return/report filed for the plan” box on their Form 5500. Prior to this, the Department identified plans as “new” if they could not be matched to a plan filing in a prior year, going back to 2001, regardless of whether they reported the filing as their first filing. Consequently, the number of “new” plans in the current Self-Insured Report to Congress is not directly comparable to the numbers reported in years prior to 2013. ↩

Based on EBSA calculations of 2022 and 2023 Form 5500 filings. ↩

See Appendix B, Tables 10 and 17. Non-plan MEWAs cover a collection of separate employee welfare benefit plans (as defined under section 3(1) of ERISA) maintained by individual employers. Because Form 5500 and 5500-SF filings do not contain direct information about participation in a non-plan MEWA, the Department assigned participation to those filings that used common plan administrator EINs and plan names. As such, any statements or statistics in this report that describe trends in participation in non-plan MEWAs likely understates true participation. ↩

Based on EBSA calculations of 2022 and 2023 Form 5500 filings. ↩

See Appendix B, Table 17. ↩

See Appendix B, Table 10. ↩

See Appendix B, Table 3. The analysis of small plan behavior over time is limited, as small plans may stop filing because their funding changed or because they terminated. ↩

See Appendix B, Table 19. ↩

For this purpose, “established plans” are those that did not indicate being initial filings in their Form 5500 or had ceased filing. ↩

See Appendix B, Table 20. ↩

See Appendix B, Tables 7 and 16. ↩

See Appendix B, Tables 7 and 16. ↩

See Appendix B, Table 7. Non-plan MEWAs cover a collection of separate employee welfare benefit plans (as defined under section 3(1) of ERISA) maintained by individual employers. Because Form 5500 and 5500-SF filings do not contain direct information about participation in a non-plan MEWA, the Department assigned participation to those filings that used common plan administrator EINs and plan names. As such, any statements or statistics in this report that describe trends in participation in non-plan MEWAs likely understates true participation. ↩

See Appendix A, Table A2. ↩

See Appendix B, Table 14. ↩

See Appendix B, Table 19. ↩

See Appendix B, Tables 2 and 17. ↩

For a discussion regarding the large plan, see page 36 of Appendix B. ↩

See Appendix A, Table Al. Note that a health-only plan does not imply that the sponsor only offers health benefits. For example, the sponsor could simultaneously offer a separate life insurance plan for which a separate Form 5500 filing exists. This report does not include information on welfare plans that do not provide health benefits. ↩

See Appendix A, Table A1. Totals do not sum due to rounding. ↩

The majority of plans indicating a funding arrangement of general assets combined with insurance filed a Schedule A (Insurance) for a nongroup health benefit. Alternatively, they were self-insured plans with stop-loss coverage or plans that check box 9a on the Form 5500 indicating insurance, but did not file a Schedule A. ↩

Totals do not sum due to rounding. There were 468 of these plans that indicated “insurance alone” as a funding arrangement in their filing but were characterized as “self-insured” for this report. However, these plans also indicated stop-loss insurance, per-capita insurance premiums consistent with an administrative services only (ASO) contract, attached a Schedule H or I that suggested a trust and self-insurance, or a combination. As a result, the Department assigned a funding mechanism of “self-insured” despite the plan indicating a funding arrangement of “insurance alone” for purposes of this report. ↩

See Appendix A, Table A7. ↩

The 217 plans that were identified as mixed-insured and indicated a trust-only funding arrangement also filed a Schedule A (Insurance) and reported a health insurance contract. Plans are deemed mixed-insured if the trust payments and the reported premium payments are more than 20 percent apart, if the percentage of participants covered by reported health insurance contracts is less than 50, or if the trust payments made directly to participants were substantial. (See Appendix B, pages 13–19) ↩

See Appendix A, Table A7. ↩

The self-insured plans that listed a benefit arrangement of the sponsor’s general assets combined with insurance may have filed a Schedule A for a nongroup health benefit or stop-loss coverage, or they may have checked box 9a on the Form 5500 indicating insurance but did not file a Schedule A. ↩

See Appendix A, Table A7. ↩

See Appendix A, Table A7. ↩

See Appendix B, Table 21. ↩

See Appendix B, Table 11. ↩

See Appendix A, Table A2. ↩

Percent changes calculated by EBSA using 2022 and 2023 Form 5500 filings. ↩

Plans that self-insure health benefits may make payments to insurance companies for administrative services, stop-loss contracts, or insurance premiums for other types of benefits (such as dental or disability). ↩

Instructions for the 2023 Form 5500, Schedule H state this category includes all payments made to other organizations or individuals providing benefits. Generally, these are individual providers of welfare benefits such as legal services, day care services, training, and apprenticeship services. ↩

See Appendix A, Tables A4 and A5. ↩

See Appendix A, Tables A4 and A5. ↩

In 2023, the Form 5500, Schedule H was updated to break out the four categories of administrative expenses reported in prior form years into 11 more specific categories, as illustrated on Schedule H, Lines 2(i)(1)-(11). See https://www.dol.gov/agencies/ebsa/employers-and-advisers/plan-administration-and-compliance/reporting-and-filing/form-5500. ↩

For filers using the 2023 Form 5500 Schedule H, the category of Professional Fees, as reported in Table A5 of Appendix A, is calculated from data reported for “Salaries and allowances” [line 2i(1)], “Recordkeeping fees” [line 2i(3)], “IQPA audit fees” [line 2i(4)], “Bank or trust company trustee/custodial fees” [line 2i(6)], “Actuarial fees” [line 2i(7)], “Legal fees” [line 2i(8)], “Valuation/appraisal fees” [line 2i(9)], and “Other trustee fees and expenses” [line 2i(10)]. For filers using earlier versions of Schedule H, the category of Professional Fees includes “Professional fees” [line 2i(1)] only. Schedule I and Form 5500-SF filers do not submit this information. ↩

Instructions for the 2023 Form 5500, Schedule H Line 2(i)(11) state that other expenses that cannot be associated definitely with lines 2(i)(1) through 2(i)(10) are reported as other administrative expenses and may include expenses for office supplies and equipment, cars, telephone, postage, rent, expenses associated with the ownership of a building used in the operation of the plan, and all miscellaneous expenses. ↩

Total for self-insured does not sum due to rounding. See Appendix A, Table A5. ↩

Total for mixed-insured does not sum due to rounding. See Appendix A, Table A5. ↩

The percentages do not sum to 100 percent due to reporting only on the categories that comprise the largest share of asset holdings. Not included are real estate, loans, assets in insurance co. general accounts, receivables, and other. ↩

DFEs are pooled investment arrangements, including master trust investment accounts, insurance company pooled separate accounts, bank common/collective trusts, other plan asset pooled investment funds (103-12 investment entities), and group insurance arrangements (GIAs). A Form 5500 must be filed for a master trust investment account. A Form 5500 is not required for the other entities, but for plans to get reporting relief with respect to those entities, the entity must file a Form 5500. Each DFE lists the plans whose assets it holds on Form 5500, Schedule D Part 2. ↩

See Appendix A, Table A6. ↩

Appendix B outlines this analysis. Bloomberg is a provider of financial and other data for private and public companies in the United States. The data include company characteristics, financial health, and financial size. Prior iterations of this report used corporate financial data from Capital IQ, which is very similar to Bloomberg data. ↩

See Appendix B, Table 23, for the distribution of the measures for each of the three categories of plans. ↩

See Appendix B, Table 4. While this is a relatively small number, many companies that filed a Form 5500 are not represented in Bloomberg data because they may be exempt from publicly issuing financial statements. Sponsors may be privately held, based overseas, or not-for-profit and without publicly issued bonds; or the plan may be a multiemployer or multiple-employer plan. ↩

See Appendix B, Table 23. Not all financial information for all employers was reported in the Bloomberg data, so the number of observations used to calculate the reported medians varies significantly. ↩

See Appendix B, Table 23. Not all financial information for all employers was reported in the Bloomberg data, so the number of observations used to calculate the reported medians varies significantly. ↩

See Appendix B, Table 23. Not all financial information for all employers was reported in the Bloomberg data, so the number of observations used to calculate the reported medians varies significantly. ↩

The Altman Z-Score is an index summarizing five financial measures that predict bankruptcy risk. ↩

See Appendix B, Figure 14. ↩